- May 27, 2026

The landscape of global remittances is undergoing a profound and necessary structural transformation. For millions of expatriates, international workers, and members of the global diaspora, financially supporting family members, managing investments, or paying for localized services in their home country is a fundamental monthly routine. Among the largest remittance corridors globally, the flow of capital back to the Indian subcontinent stands out as a critical economic driver. However, for decades, consumers have been forced to rely on an antiquated, fragmented, and highly expensive traditional banking system.

When individuals look for modern solutions to send money to India, their primary concerns invariably revolve around two critical metrics: the total financial cost of the transaction and the speed of delivery. The legacy financial infrastructure—characterized by multi-day delays, unpredictable correspondent banking deductions, and heavily inflated currency conversion margins—no longer serves the best interests of the modern consumer. Today, a new paradigm has emerged, driven by the convergence of India's highly advanced Unified Payments Interface (UPI) and innovative financial technologies such as peer-to-peer (P2P) matching. This comprehensive guide will deeply analyze the hidden flaws of traditional cross-border payments, deconstruct the revolutionary local compensation model utilized by platforms like CashSwap Club, and provide a detailed roadmap for executing instant, secure, and highly cost-effective international transfers.

1. The Structural Inefficiencies and Hidden Costs of Traditional Banking

To fully appreciate the value of modern fintech alternatives, it is essential to first understand the systemic bottlenecks inherent in conventional banking networks. The vast majority of traditional cross-border transactions are routed through the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network. Established over fifty years ago, SWIFT was engineered as a secure messaging protocol for institutional communication, not as a rapid clearinghouse for retail consumer transactions. When an individual initiates a standard international wire transfer, the capital does not move directly from the originating account to the destination bank in India.

The Burden of Correspondent Banking Networks

Instead of a direct transfer, the transaction must navigate a complex, multi-layered web of intermediary or correspondent banks. Each institution in this chain processes the transaction sequentially, and crucially, each bank acts as an independent entity seeking profitability. Consequently, these intermediary banks frequently deduct processing fees directly from the principal transfer amount. This practice leads to a highly unpredictable financial outcome; the sender cannot guarantee the exact sum that will ultimately reach the beneficiary's account. For families relying on precise amounts to cover medical expenses, tuition fees, or real estate down payments, this unpredictability creates significant logistical challenges. Furthermore, because each node in the network requires verification, processing times routinely stretch from three to five business days, rendering the system entirely unsuitable for emergency financial support.

The Reality of Exchange Rate Manipulation

Beyond explicit processing deductions, the most substantial financial loss incurred by consumers stems from opaque currency conversion practices. Global financial institutions trade currencies among themselves using the interbank exchange rate—the true, real-time market value of a currency pair. However, retail consumers are almost never granted access to this baseline rate. Traditional banks and legacy money transfer operators systematically apply a markup or "spread" to the exchange rate, artificially deflating the value of the sender's currency. This hidden margin often ranges between 2% and 6%, functioning as an invisible tax that erodes the purchasing power of the transferred funds. Recognizing these inflated transfer fees is the first step toward financial empowerment, highlighting the urgent need for a transparent alternative that prioritizes the user's financial equity over institutional profit margins.

2. Deconstructing Peer-to-Peer Matching and Local Compensation

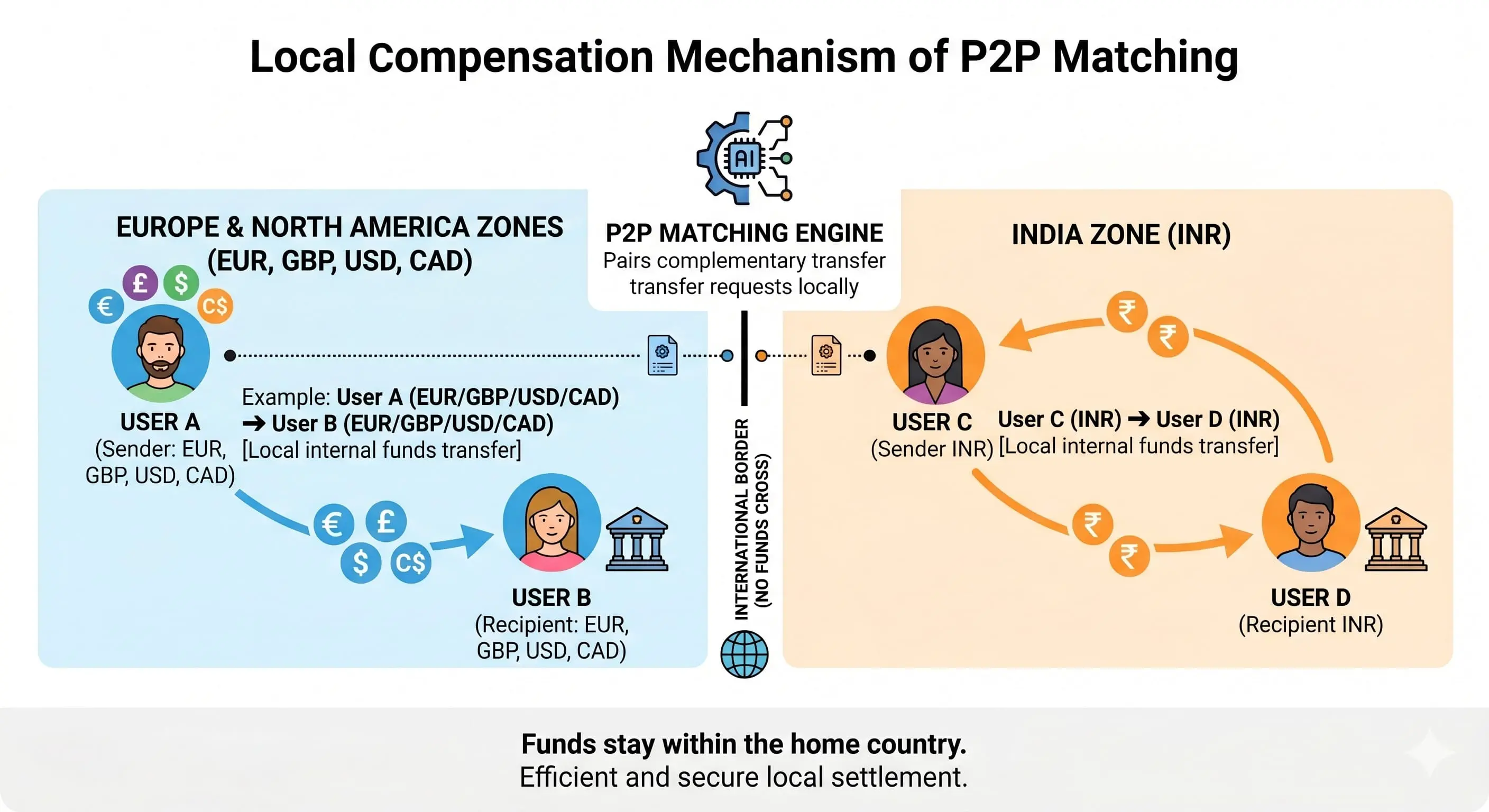

The definitive solution to the archaic SWIFT infrastructure lies in a complete architectural redesign of how capital is handled across borders. CashSwap Club operates on a fundamentally different premise known as Peer-to-Peer (P2P) matching, supported by a system of local compensation. This model completely bypasses international routing networks because, under this framework, the money never actually crosses a geographical or digital border. Instead, the marketplace intelligently matches reciprocal financial needs within isolated, local ecosystems.

The Mechanics of Local Compensation

Consider a scenario where a user in Europe wishes to send funds to a relative in India. In a P2P matching system, the European user deposits their Euros into the platform's secure, localized European account. Simultaneously, the platform's algorithmic matching engine identifies an inverse request—for instance, an individual or business in India looking to send Indian Rupees to Europe. The platform executes a local settlement: the European Euros are used to fulfill the payout required by the user sending money to Europe, while the Indian Rupees already present within the platform's Indian liquidity pool are instantly routed to the initial sender's beneficiary in India. All financial movements remain strictly domestic.

Achieving True Financial Transparency

The implications of this closed-loop architecture are monumental. By eliminating the necessity for funds to traverse international jurisdictions, the platform bypasses all correspondent banking fees and international regulatory frictions. More importantly, because the platform does not need to purchase currency on the open wholesale market to fulfill the transfer, it can offer users the absolute, unmodified interbank exchange rate. There are no hidden margins, no spreads, and no opaque deductions. Users are subject only to a minimal, clearly defined, flat operational fee. This commitment to total transparency reflects a broader movement towards financial democratization. Individuals looking to understand the core philosophy behind this equitable model can embrace the foundational manifesto and the commitment to a fairer global economy.

Furthermore, relying on community-driven liquidity creates a highly efficient, self-sustaining financial ecosystem that rewards all participants with better rates. For a deeper technical understanding of why this model consistently outperforms traditional banking corridors, users are encouraged to discover exactly why peer-to-peer technology is revolutionizing the global remittance landscape.

3. Navigating the Indian Digital Ecosystem: UPI, Mobile Wallets, and Major Banks

The speed and efficiency of a P2P matching network are only as effective as the domestic payment rails in the destination country. Fortunately, India possesses one of the most sophisticated, high-velocity digital payment infrastructures in the world. The cornerstone of this ecosystem is the Unified Payments Interface (UPI). Developed by the National Payments Corporation of India (NPCI) and regulated by the Reserve Bank of India (RBI), UPI enables instant, real-time interbank transactions directly from a mobile device.

The Power of Instant Settlements

UPI has revolutionized the way money moves within India. Instead of requiring complex account numbers and branch-specific IFSC codes, UPI utilizes a simple Virtual Payment Address (VPA), which is often linked directly to the user's mobile phone number or email address. When the P2P matching engine completes its local compensation process, the platform triggers a domestic UPI payout. Because UPI operates 24 hours a day, 7 days a week, 365 days a year, the funds are credited to the beneficiary's account within seconds, completely immune to traditional banking hours, weekends, or public holidays. This integration definitively solves the historical problem of delivery delays.

Seamless Integration with Dominant Mobile Wallets

The widespread adoption of UPI is heavily driven by third-party application providers that dominate the Indian retail market. Applications such as Paytm, PhonePe, and Google Pay India have become the primary financial interfaces for hundreds of millions of citizens. A premium remittance platform must offer native, frictionless integration with these applications. Senders can simply input their family member's PhonePe number or Google Pay India ID, and the matched funds are delivered instantly to the linked bank account, ready for immediate withdrawal or digital spending. Additionally, robust connectivity with India's largest financial institutions—including the State Bank of India (SBI), HDFC Bank, and ICICI Bank—ensures that larger capital transfers are settled with maximum reliability and institutional security.

4. Regulatory Nuances for the Diaspora: NRE vs. NRO Accounts

For Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) managing cross-border wealth, understanding the regulatory framework enforced by the Foreign Exchange Management Act (FEMA) is absolutely critical. Indian banking regulations stipulate that expatriates cannot maintain standard domestic savings accounts. Instead, they must route their funds through specialized account structures: specifically, Non-Resident External (NRE) and Non-Resident Ordinary (NRO) accounts. Differentiating between these two accounts is vital for optimizing tax liabilities and ensuring seamless fund repatriation.

Non-Resident External (NRE) Accounts: Total Repatriability

An NRE account is specifically designed to hold foreign earnings that are transferred into India. These accounts are denominated in Indian Rupees, but the capital must originate from a foreign jurisdiction. The primary advantage of the NRE account is its complete repatriability. The account holder can freely transfer the principal amount, along with any accrued interest, back to their country of residence without any regulatory caps or permissions. Crucially, the interest earned on the balance of an NRE account is entirely exempt from Indian income tax. This makes it the ideal vehicle for expatriates looking to build tax-free savings or fund large-scale investments in the Indian market.

Non-Resident Ordinary (NRO) Accounts: Managing Domestic Yields

Conversely, an NRO account is strictly intended for managing income generated within India. This includes domestic revenue streams such as rental income from Indian real estate, dividends from the Bombay Stock Exchange, or pension payouts. While foreign funds can be deposited into an NRO account, it is generally unadvisable due to differing tax treatments. Interest earned on an NRO account is fully taxable in India and is subject to Tax Deducted at Source (TDS). Furthermore, the repatriation of funds from an NRO account is heavily restricted, currently capped at one million USD per financial year, and requires extensive certification from a chartered accountant. Using the best transfer app allows the diaspora to consciously direct their hard-earned foreign capital directly into NRE accounts, protecting their wealth from unnecessary taxation while ensuring complete liquidity.

5. Step-by-Step Guide: Executing Seamless Platform Transfers

Transitioning away from traditional banks to a modern P2P marketplace is a straightforward process designed to prioritize user experience and transparency. Here is a detailed breakdown of the operational workflow when initiating a transfer:

- Step 1: Secure Registration and Identity Verification. The user creates an account on the application. To comply with global financial regulations, a rapid, automated verification process requires the upload of official identification to establish a secure, trusted profile.

- Step 2: Defining Transaction Parameters. The user inputs the exact amount they wish to send in their local currency (e.g., EUR, GBP, USD) and selects INR as the destination currency. The interface instantly displays the live interbank exchange rate and the flat, transparent fee. The exact payout amount is clearly shown, ensuring zero surprises for the beneficiary.

- Step 3: Entering Beneficiary Details. The sender provides the recipient's information. For maximum efficiency, this involves entering the recipient's UPI ID associated with Paytm, PhonePe, or Google Pay India. Standard bank details (Account Number and IFSC code) for institutions like SBI, HDFC, or ICICI can also be used.

- Step 4: Funding the Local Pool. The sender transfers the designated amount into the platform's secure, localized bank account using a domestic payment method (such as a SEPA transfer in Europe, ACH in the US, or Faster Payments in the UK). This local deposit incurs no international fees.

- Step 5: Algorithmic Matching and Instant Delivery. Upon receipt of the domestic funds, the matching engine pairs the transaction with reciprocal liquidity in India. The platform instantly triggers a local UPI payout, crediting the beneficiary's account in real-time, accompanied by an immediate digital confirmation.

6. Security Infrastructure, Regulatory Compliance, and KYC Protocols

In the realm of digital finance, the preservation of user trust is paramount. A decentralized peer-to-peer matching network requires an uncompromising security infrastructure to protect user capital and ensure the integrity of the platform across multiple international jurisdictions. Compliance is not merely a legal checkbox; it is the structural foundation of the marketplace.

Rigorous Know Your Customer (KYC) Standards

To maintain a secure environment, the platform strictly enforces comprehensive Know Your Customer (KYC) protocols. Every participant must undergo biometric and documentary identity verification before gaining access to the matching engine. This mandatory screening prevents fraudulent accounts, stops identity theft, and ensures that the platform is utilized exclusively by verified, legitimate users. By maintaining a pristine user base, the platform safeguards the collective financial health of the community.

Advanced Anti-Money Laundering (AML) and Fund Safeguarding

Simultaneously, state-of-the-art Anti-Money Laundering (AML) algorithms continuously monitor all network activity. These systems analyze transaction patterns, velocity, and volumes in real-time, cross-referencing global sanctions lists to preemptively block illicit financial flows. Furthermore, to guarantee ultimate capital security, all user funds are strictly segregated from the platform's corporate operational accounts. User deposits are held in safeguarded, tier-one banking institutions within their respective local jurisdictions. This strict segregation ensures that user capital is never subjected to corporate risk, speculative investment, or institutional illiquidity, providing absolute peace of mind from the moment a deposit is made until the final payout is confirmed.

7. Conclusion: The Transition to Transparent Financial Corridors

The era of accepting punitive deductions, opaque conversion margins, and agonizing delays for international remittances is definitively over. The convergence of localized peer-to-peer matching engines with the unparalleled speed of the Indian UPI ecosystem has created a superior, frictionless alternative to the legacy banking system. Expatriates and international workers no longer need to sacrifice a significant portion of their hard-earned income to sustain the overhead of traditional correspondent banks.

By keeping capital flows strictly domestic, platforms like CashSwap Club deliver an unprecedented level of efficiency. Users gain absolute clarity on costs, access to the true interbank market rate, and the assurance that their families will receive funds instantly via familiar platforms like Paytm, PhonePe, or Google Pay India. It is time to reclaim the full value of your international earnings. Take control of your cross-border finances today, test the live rate simulator, and experience the unparalleled speed and transparency of the modern P2P remittance network.

Frequently asked questions

How long does a transfer to an Indian account via UPI take?

Thanks to the efficiency of the P2P matching system and the real-time processing capabilities of the Indian Unified Payments Interface (UPI), transfers are exceptionally fast. Once the matching engine completes the local compensation, funds are typically credited to the recipient's UPI-linked bank account or mobile wallet (such as PhonePe or Google Pay India) within seconds to a few minutes.

Are there any hidden margins on the exchange rate?

No. The fundamental principle of the P2P matching model is absolute transparency. The platform strictly applies the real-time interbank exchange rate—the same rate seen on global financial markets. There are zero hidden markups or spreads; users pay only a clearly stated, minimal fixed fee for the platform's matching service.

Is the P2P money transfer model legal and secure?

Absolutely. The platform operates in strict accordance with international financial regulations and holds the necessary licenses for payment processing in its respective jurisdictions. It utilizes mandatory KYC (Know Your Customer) identity verification, AML (Anti-Money Laundering) monitoring, and bank-grade encryption to ensure the highest level of security and compliance for every user.

Can funds be sent directly to an NRE or NRO account?

Yes. The platform supports direct transfers to major Indian financial institutions including SBI, HDFC, and ICICI. Users can specify whether the destination is an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account, allowing members of the diaspora to manage their tax-free repatriable funds or local income securely and efficiently.

Peer-to-peer currency exchange, finally simple and fair.

Our peer-to-peer currency exchange and money transfer platform is currently under development. We are preparing a solution that will allow you to exchange currencies with a seamless and secure experience.

To be among the first to know and not miss anything about the launch, join the club by subscribing to our newsletter.

Visuals disclosure : In the interest of transparency, please note that the images illustrating this article were created using artificial intelligence (AI) generation tools.