The contemporary global economy is defined by an unprecedented mobility of people, ideas, and capital. In this deeply interconnected landscape, cross-border financial flows have evolved from niche banking operations into vital economic lifelines. For millions of households worldwide, international remittances represent essential support for daily expenses, education, healthcare, and real estate investments. Similarly, freelancers, independent contractors, and digital entrepreneurs routinely rely on seamless cross-border payments to sustain their businesses and collaborate with international clients. Despite this exponential growth in demand, the traditional financial architecture has largely failed to keep pace with the needs of modern society. For decades, legacy banks and conventional money transfer operators have maintained an expensive, slow, and opaque monopoly over global fund movements.

However, the rise of financial technology (Fintech) is fundamentally reshaping this paradigm. Among the most disruptive innovations in this space is the Peer-to-Peer (P2P) matching model. By shifting away from centralized, bureaucratic banking corridors and moving toward decentralized, community-driven networks, P2P architecture offers a radical alternative to old-world systems. This comprehensive analysis explores the macroeconomic dynamics of global remittances, exposes the structural flaws of traditional banking institutions, and explains why peer-to-peer marketplaces—such as CashSwap Club—represent the future of transparent, secure, and cost-effective international money movement.

To fully appreciate the advantages of peer-to-peer technology, one must first examine the inherent inefficiencies of the legacy banking system. For over half a century, international bank wires have relied almost exclusively on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network. While SWIFT succeeded in establishing a standardized messaging system for financial institutions, its underlying operational mechanics are fundamentally outdated, costly, and unsuited for the digital age.

A common misconception among consumers is that a traditional international bank wire moves money directly from the sender’s account to the recipient’s account across borders. In reality, the process is far more convoluted. Because most banks do not maintain direct relationships with every other financial institution worldwide, they must rely on an intermediary network known as correspondent banking. When a transfer is initiated, the funds must travel through a chain of multiple intermediary banks before reaching their final destination.

Each intermediary bank along this chain operates as an independent entity, introducing its own administrative protocols, clearing delays, and processing fees. These intermediary charges are frequently deducted directly from the principal amount without prior notification to the sender. Consequently, achieving true transfer transparency becomes impossible within the traditional framework. Senders are left unable to predict exactly how much money will arrive in the recipient's account, or when it will get there. This multi-layered processing routinely extends delivery times to three to five business days, an unacceptable delay in an era where data moves instantaneously.

While upfront administrative commissions are frustrating, the most significant financial penalty imposed by traditional institutions is found within the exchange rate markup. Legacy financial providers rarely give retail clients access to the real interbank exchange rate—the mid-market rate utilized by large corporations and financial institutions on global markets. Instead, they apply a heavily distorted, unfavorable exchange rate, pocketing the difference as an additional profit margin.

These frais cachés banques (hidden bank fees) mean that a bank might advertise a deceptively low flat fee to attract customers, while quietly extracting between 3% and 8% of the total transaction value through an artificially inflated exchange rate. For families reliant on remittances, or small businesses operating on thin margins, these hidden charges represent a massive drain on capital. A thorough comparatif transfert argent (money transfer comparison) consistently reveals that traditional banks remain the most expensive and least equitable option for global fund movement, penalizing users who lack specialized financial knowledge.

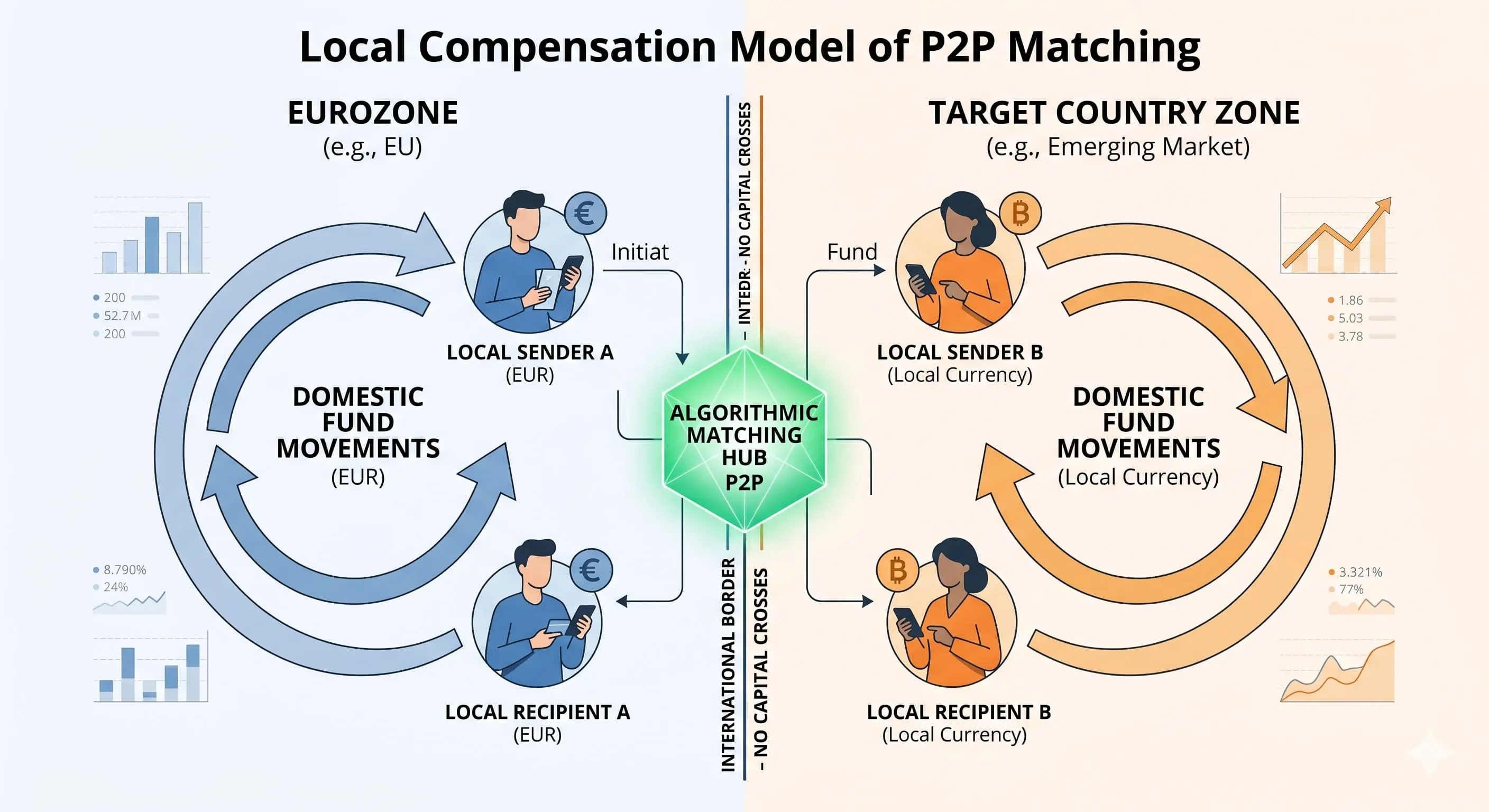

In direct response to the systemic friction of legacy banking, peer-to-peer financial technology introduces a paradigm shift based on an elegant economic principle: the most efficient way to transfer money across borders is to ensure that the money never actually crosses a border. By bypassing the physical and institutional boundaries that slow down traditional finance, P2P marketplaces completely rewrite the rules of global remittances.

Platforms built on peer-to-peer architecture, such as CashSwap Club, function as intelligent digital matching engines. Instead of routing funds through expensive international corridors, these platforms synchronize opposite, complementary directional needs within a global user network. For instance, if an individual located in Europe intends to send funds to a recipient in a target country (e.g., in Africa, Asia, or Latin America), the platform’s algorithm simultaneously identifies an independent user in that target country who needs to send an equivalent amount back to Europe.

Rather than executing a complex cross-border transaction, the system orchestrates a dual localized settlement:

Because all actual fund movements are domestic, the money never leaves its country of origin. This reliance on local clearing networks entirely eliminates intermediary correspondent banks, minimizes operational friction, and radically accelerates processing times.

By restricting all financial transactions to local networks, P2P marketplaces remove the foreign exchange risks and conversion costs that traditional banks use to justify their steep markups. Free from these structural burdens, a true P2P platform can offer its users the real interbank exchange rate without any hidden spreads.

The platform's revenue model is completely transparent, relying solely on a minimal, clearly defined fixed fee disclosed upfront before the user commits to the transaction. This level of honesty guarantees that senders know exactly what they are paying, and recipients know down to the exact cent what they will receive. By maximizing the amount of money successfully delivered to destination countries, P2P platforms directly enhance the financial well-being of families and local communities worldwide.

Transitioning from traditional banking networks to a peer-to-peer digital marketplace is a seamless, user-centric experience. By stripping away legacy bureaucracy, P2P web and mobile applications provide an accessible interface that allows users to manage international transfers with total confidence and minimal effort.

The process begins by accessing the P2P marketplace via its smartphone application or official website. Registration requires only a few moments to set up basic login credentials. To ensure absolute compliance with global financial regulations, the platform initiates a streamlined identity verification process. Users simply upload a valid government-issued ID and complete a quick, automated biometric check. This foundational step is critical to maintaining a trustworthy, fraud-free ecosystem for all participants.

Once the account is verified, the user enters the desired transfer amount and selects the destination currency. The platform's live simulator instantly displays the current interbank exchange rate, the precise fixed fee, and the exact amount the recipient will receive. There are no unexpected deductions or delayed calculations; the numbers shown during the simulation are guaranteed, providing total financial clarity from the outset.

After confirming the simulated terms, the sender funds the transfer using a convenient domestic payment method, such as a local bank transfer or a debit card. Once the deposit is received, the platform's matching engine automatically pairs the transaction with complementary flows moving in the opposite direction. Because the network processes substantial volumes globally, this matching process occurs behind the scenes without requiring manual intervention from the user.

As soon as the match is confirmed, the corresponding funds are unlocked locally in the destination country and dispatched to the recipient. Senders frequently ask: 'How much will it cost and how fast will my family receive the money?' Through a P2P architecture, the cost is restricted to the tiny, transparent fixed fee shown at the start, and the delivery time is remarkably fast—often settling instantly or within less than 24 hours. The recipient can choose to receive the capital directly into their traditional bank account or via a Mobile Money wallet, a highly popular option that provides instant utility in regions with low banking density.

A natural and necessary question for anyone adopting innovative financial technology relates to safety. The term "peer-to-peer" can sometimes be misunderstood as an informal or unregulated arrangement. In reality, licensed P2P financial platforms operate under strict regulatory supervision, deploying advanced security protocols identical to—and often exceeding—those used by major international commercial banks.

Maintaining uncompromised sécurité financière (financial security) is the absolute priority of any reputable peer-to-peer financial marketplace. Every participant on the platform must undergo a rigorous Know Your Customer (KYC) screening process to prevent identity theft and account fraud. Furthermore, P2P platforms integrate state-of-the-art automated monitoring systems powered by machine learning. These algorithms analyze transactional metadata in real time to detect abnormalities, flags potential risks, and actively prevent money laundering and terrorist financing (AML/CFT), ensuring a completely clean and trustworthy ecosystem.

To operate legally, a peer-to-peer money transfer marketplace must hold formal authorizations as a regulated payment institution. Platforms like CashSwap Club operate under licenses granted by top-tier financial regulators, such as the ACPR in France, the FCA in the United Kingdom, or equivalent banking authorities worldwide. These regulatory frameworks require strict adherence to capital reserve mandates, regular independent audits, and rigid data privacy standards in line with the GDPR.

Crucially, user funds are protected through a process known as safeguarding. Senders' deposits are never absorbed into the platform’s operational bank accounts; instead, they are held in separate, isolated escrow accounts managed by major global custodian banks. This means that even in the highly unlikely event that the tech platform faces operational difficulties, the users' capital remains completely untouched, secure, and fully refundable under international law.

The traditional cross-border payment system—characterized by heavy bureaucracy, lengthy delays, and hidden costs—is no longer viable in our fast-moving digital world. Choosing a peer-to-peer model for international transfers means breaking free from predatory bank spreads and unnecessary intermediary networks. By leveraging local clearing mechanisms and smart algorithmic matching, P2P technology hands financial control back to the consumer, offering real exchange rates and fast execution speeds built for modern life.

Beyond the undeniable financial savings, utilizing a P2P marketplace represents a conscious decision to support a fairer, more community-driven global economy. To explore the ethical foundations and long-term vision driving this financial shift, users can read the manifesto for an equitable and transparent financial system. To experience this financial evolution firsthand and see exactly how much you can save on your next international transfer, explore the live rate simulator today.

While traditional banks require three to five business days to process cross-border wires due to the complexities of the SWIFT network, P2P platforms rely on domestic clearing systems. Consequently, once your transfer is automatically matched by the algorithm, funds are typically delivered to the recipient’s bank account or Mobile Money wallet almost instantly, or within a maximum window of 24 hours.

Yes, utilizing a licensed peer-to-peer marketplace is entirely legal and highly secure. These platforms operate as authorized payment institutions under the direct supervision of national central banks and major financial conduct authorities. They enforce strict identity verification (KYC), employ bank-grade data encryption, and safeguard all user funds in dedicated custodian accounts.

Unlike traditional banks that profit from hidden exchange rate markups, P2P platforms offer complete transparency. All transactions are converted using the real, mid-market interbank exchange rate. The platform charges only a single, low fixed fee that is clearly displayed to the user before the transaction is finalized, ensuring there are no surprise deductions at delivery.

High-volume P2P marketplaces manage vast networks of continuous global transactions, making unmatched requests rare. However, to guarantee uninterrupted service, platforms maintain pre-funded local currency reserves and partner with institutional liquidity providers. If a retail peer match is not instantly available, these liquidity backstops automatically step in to process your transfer without causing any operational delays for the recipient.

Our peer-to-peer currency exchange and money transfer platform is currently under development. We are preparing a solution that will allow you to exchange currencies with a seamless and secure experience.

To be among the first to know and not miss anything about the launch, join the club by subscribing to our newsletter.

Visuals disclosure : In the interest of transparency, please note that the images illustrating this article were created using artificial intelligence (AI) generation tools.

© CashSwap Club 2026 - All rights reserved

Designed with ❤️ in Paris • Made in France 🇫🇷

French

French  Spanish

Spanish