- Jun 26, 2026

The global landscape of international remittances is undergoing a massive transformation, particularly for funds directed toward East Africa. For members of the diaspora looking to send money to Kenya, the priority remains clear: ensuring that funds reach families, businesses, and communities as quickly and cost-effectively as possible. Historically, international wire transfers have been plagued by sluggish processing times, opaque exchange rate markups, and excessive intermediary fees. Today, technological advancements have paved the way for more equitable solutions.

Among these solutions, the Peer-to-Peer (P2P) matching model stands out as a revolutionary approach to financial clearing. By completely bypassing traditional banking corridors and connecting multi-currency digital wallets, modern platforms empower users to bypass systemic inefficiencies. This comprehensive guide explores the mechanics of P2P matching, the vital role of the Kenyan mobile money ecosystem, and how individuals can optimize their international transfers to guarantee maximum value for every cent remitted.

Table of Contents

- The True Cost of Remittances: Traditional Banks vs. Modern Marketplaces

- Understanding Kenya's M-Pesa and Mobile Money Ecosystem

- How P2P Matching Revolutionizes International Transfers

- Step-by-Step Guide: Transferring Funds on CashSwap Club

- Security, Compliance, and Community Trust

- Conclusion: Empowering the Diaspora with Transparent Transfers

- Frequently Asked Questions

The True Cost of Remittances: Traditional Banks vs. Modern Marketplaces

For decades, traditional financial institutions have maintained a monopoly over cross-border capital flows. When individuals initiate a standard international wire transfer, the funds do not travel in a straight line. Instead, they navigate the SWIFT network, bouncing between multiple correspondent and intermediary banks. Each node in this complex chain exacts a toll, systematically reducing the final amount that reaches the beneficiary.

The most pervasive issue within this traditional framework is the lack of transparency regarding the exchange rate. Banks rarely offer the mid-market rate—the genuine, real-time rate at which banks trade currencies with one another. Instead, a hidden margin is baked directly into the retail exchange rate. Consequently, senders pay an invisible tax on their own capital. Furthermore, fixed transfer fees, receiving fees, and correspondent deductions compound the overall expense, making small, regular remittances highly uneconomical.

To fully grasp the magnitude of these systemic inefficiencies, it is crucial to identify and avoid hidden bank fees on global money transfers. The shift toward decentralized marketplaces represents a necessary evolution. By eliminating the middleman, the financial paradigm shifts from corporate profit maximization to community-driven efficiency. To dive deeper into this industry shift, one can explore the battle of hidden transfer fees between marketplaces and traditional banks, illustrating exactly why the legacy correspondent banking system is becoming obsolete for personal remittances.

Understanding Kenya's M-Pesa and Mobile Money Ecosystem

In Kenya, the concept of a bank account has been radically redefined over the last fifteen years. Safaricom's M-Pesa is not merely a financial product; it is the fundamental infrastructure of the Kenyan economy. For the diaspora looking to send money to Kenya, understanding this ecosystem is absolutely mandatory. While traditional banking institutions like Kenya Commercial Bank (KCB), Equity Bank, and NCBA Bank play critical roles in corporate finance and large-scale asset management, daily life runs almost entirely on Mobile Money.

When funds land directly in an M-Pesa wallet, the recipient gains immediate, frictionless purchasing power. Mobile money represents the primary economic lifestyle in Kenya. Upon receiving funds, individuals can instantly pay electricity and water bills (via paybills for entities like KPLC), settle rent, pay school fees, or purchase groceries at local markets using the 'Lipa na M-Pesa' functionality. There is no need to travel to a bank branch, wait in line, or carry physical cash—processes that are time-consuming and pose security risks.

Furthermore, local banks have deeply integrated with mobile network operators. Accounts at Equity Bank or KCB can be linked directly to M-Pesa lines, allowing for fluid domestic movement of capital. Therefore, the most efficient transfer method is one that deposits value directly into this mobile ecosystem. Platforms connecting global currencies directly to Kenyan Shillings (KES) within the M-Pesa network ensure that beneficiaries experience zero friction between the moment funds are sent and the moment they are utilized for daily necessities.

How P2P Matching Revolutionizes International Transfers

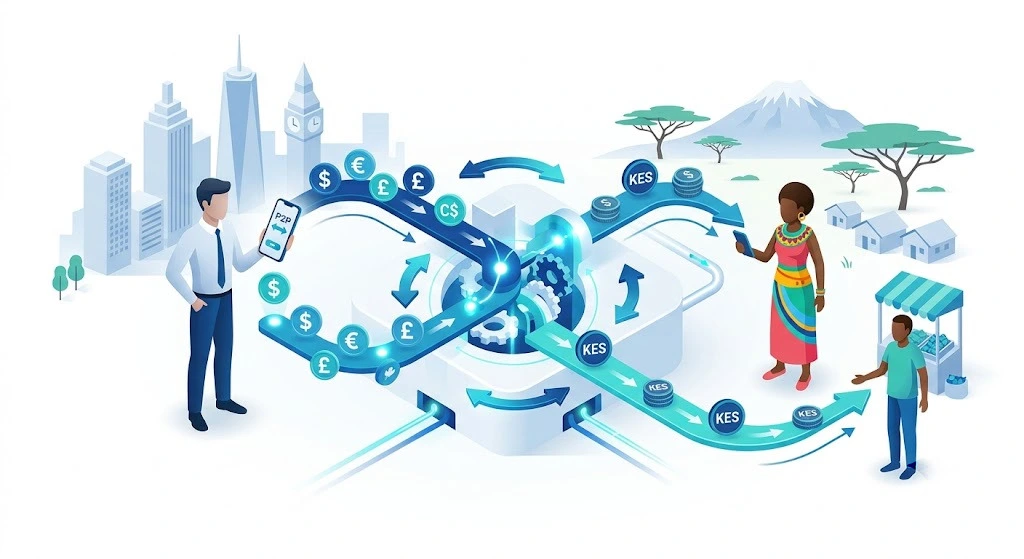

The core technological breakthrough solving the remittance problem is the Peer-to-Peer (P2P) matching marketplace. CashSwap Club operates precisely on this model, ensuring that fiat currency never actually physically crosses international borders. This localized clearing system represents a paradigm shift in global finance.

The mechanism functions by matching the opposing financial needs of two independent users. The platform hosts multi-currency wallets, supporting major global currencies such as Euros (EUR), US Dollars (USD), British Pounds (GBP), and Canadian Dollars (CAD). When a user in Europe wishes to send money to Kenya, they do not execute a SWIFT wire. Instead, they deposit Euros into their secure, platform-hosted EUR wallet. The platform’s matching engine then locates another user who holds Kenyan Shillings locally in Kenya but desires Euros in Europe.

The transaction is settled locally on both ends. The Kenyan Shillings are transferred via domestic rails—such as an instant M-Pesa transfer—directly to the beneficiary. Simultaneously, the Euros are transferred between the internal multi-currency wallets on the platform. Because the money does not traverse international banking corridors, the users avoid SWIFT fees, intermediary deductions, and opaque currency conversion markups. The matching system guarantees the real interbank exchange rate, applying only minimal, transparent, and fixed platform fees. It is highly recommended to understand why choosing P2P for money transfers is highly advantageous for those making regular remittances.

In a volatile global economy, exchange margins can severely deplete transferred wealth. Individuals utilizing P2P networks can learn why exchange rates fluctuate and how to beat the market by relying on direct user-to-user matching rather than institutional rate-setting.

Step-by-Step Guide: Transferring Funds on CashSwap Club

Executing a transfer using a P2P marketplace is designed to be intuitive, ensuring that even individuals with minimal technical expertise can navigate the process seamlessly. Here is the detailed breakdown of how to send money to Kenya using the CashSwap Club platform.

Step 1: Account Creation and Verification (KYC)

Before any financial activity can occur, users must create a secure profile. Regulatory compliance dictates that all participants undergo a Know Your Customer (KYC) verification process. This involves submitting a valid, government-issued identification document and proof of address. This step is non-negotiable and serves to protect the entire community from illicit activities.

Step 2: Funding the Multi-Currency Wallet

Once verified, the user funds their digital wallet in their local fiat currency (e.g., EUR, USD, GBP, or CAD). This is typically done via a standard, free domestic bank transfer (such as SEPA in Europe). Since this is a domestic transfer to the platform's regional account, no international fees apply.

Step 3: Initiating the Matching Request

With the wallet funded, the user creates a transfer request, specifying the target amount in Kenyan Shillings (KES) and providing the beneficiary's exact M-Pesa mobile number or local bank details (e.g., Equity Bank, KCB). The platform’s algorithm calculates the exact interbank exchange rate and displays the transparent, fixed platform fee before confirmation.

Step 4: The P2P Match and Local Clearing

The algorithm matches the request with an opposing user. The counterpart fulfills the local side of the transaction by sending the KES directly to the provided M-Pesa number. Once the beneficiary confirms receipt of the exact funds on their mobile device, the platform releases the locked foreign currency (e.g., EUR) from the sender’s wallet to the counterpart’s wallet.

Step 5: Mandatory Mutual Evaluation

To finalize the process, both users must evaluate the transaction. This mandatory rating system enforces strict accountability, ensuring that only reliable, fast, and communicative participants remain active within the marketplace.

Security, Compliance, and Community Trust

When dealing with international finance, security is the paramount concern. A P2P marketplace must go beyond simple technological encryption to foster genuine trust among its user base. CashSwap Club addresses this through rigorous compliance frameworks and community-driven self-regulation.

The platform adheres strictly to Anti-Money Laundering (AML) directives and international financial regulations. The KYC procedure ensures that every single participant on the network is fully identified and vetted. While the transactions are peer-to-peer, the environment is highly moderated and monitored for suspicious activities. Users must remain vigilant, and it is beneficial to adopt the five essential reflexes to protect online financial transactions to maintain personal security hygiene.

Furthermore, the structural design of the platform eliminates counterparty risk during the exchange. Funds within the multi-currency wallets are securely locked (escrowed) by the system the moment a match is initiated. They are only released once the off-platform domestic transfer (the M-Pesa receipt) is definitively confirmed. If a dispute arises, the platform's arbitration team steps in to review the cryptographic proofs and local transfer receipts, guaranteeing that no user loses their capital.

The mandatory mutual rating system acts as a powerful behavioral incentive. Users are heavily motivated to execute their local transfers swiftly and accurately to maintain a high trust score. A poor rating instantly affects a user's ability to participate in future matches, creating a highly efficient, self-regulating ecosystem built entirely on transparency and solidarity.

Conclusion: Empowering the Diaspora with Transparent Transfers

The methodology for sending funds across borders has irrevocably changed. The heavy fees, unfavorable exchange rates, and slow processing times associated with traditional banking networks are no longer an unavoidable reality. By leveraging the power of M-Pesa in Kenya and the innovative mechanics of P2P matching, the diaspora can now support their families and manage investments with unprecedented efficiency.

Financial inclusion means having access to the real value of one's money. Platforms utilizing multi-currency wallets and local clearing networks ensure that capital serves the people, not the intermediary institutions. To join this financial revolution, users can discover the core values driving transparent financial matching and subsequently access the primary P2P money transfer platform to run a live simulation of the current interbank rates.

Frequently asked questions

How long does a transfer to M-Pesa take using P2P matching?

Because the local transaction occurs entirely within domestic networks, transfers are typically completed within minutes once a match is found. As soon as the counterpart executes the local mobile money transfer, the funds reflect instantly in the recipient's M-Pesa balance, bypassing the multi-day delays of international SWIFT wires.

Is sending money via a P2P marketplace safe and legal?

Yes. Reputable P2P platforms operate under strict financial regulations, enforcing comprehensive Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols. Furthermore, the escrow-like locking mechanism of the multi-currency wallets ensures that funds are only released when the receipt of local currency is verified.

What exchange rate will be applied to the transfer?

Unlike traditional banks that apply a hidden markup, P2P matching platforms utilize the real mid-market exchange rate (the interbank rate). Users bypass institutional currency conversion margins entirely, ensuring the beneficiary in Kenya receives the maximum possible amount in Shillings (KES).

Can transfers be sent to Kenyan bank accounts instead of M-Pesa?

Absolutely. While M-Pesa is the most popular and instantaneous method for daily transactions, users can also specify local banking details. Counterparts can fulfill the match by executing domestic transfers to local institutions such as Kenya Commercial Bank (KCB), Equity Bank, or NCBA Bank.

Peer-to-peer currency exchange, finally simple and fair.

Our peer-to-peer currency exchange and money transfer platform is currently under development. We are preparing a solution that will allow you to exchange currencies with a seamless and secure experience.

To be among the first to know and not miss anything about the launch, join the club by subscribing to our newsletter.

Visuals disclosure : In the interest of transparency, please note that the images illustrating this article were created using artificial intelligence (AI) generation tools.