In an increasingly interconnected global economy, the flow of capital across borders serves as the lifeblood for millions of families, small businesses, and local economies. Sending money to the Dominican Republic—and to emerging markets worldwide—has historically been dominated by traditional financial institutions and monopolistic remittance operators. These legacy entities have constructed complex, opaque networks that systematically erode the value of the funds being transferred. For individuals seeking to support relatives, manage international investments, or settle cross-border obligations, understanding the mechanics of international finance is no longer optional; it is an economic necessity.

The core question that drives every sender is fundamentally simple: how much will the transaction cost, and how rapidly will the recipient access the funds? Unfortunately, the traditional banking sector obfuscates the answer through convoluted pricing structures and inefficient routing systems. A paradigm shift is occurring, driven by decentralized methodologies and peer-to-peer (P2P) matching technologies. This comprehensive guide dissects the architectural flaws of traditional remittances and explores how modern marketplace models, specifically CashSwap Club, provide a mathematically superior alternative for optimizing exchange rates and eliminating systemic inefficiencies.

To fully appreciate the innovation brought by marketplace models, it is essential to deconstruct the legacy systems that currently process the majority of international transactions. When capital is sent from North America or Europe to the Dominican Republic, it rarely travels directly from the sender's institution to the receiver's local bank. Instead, it enters the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network, navigating a labyrinth of correspondent banks.

Each correspondent bank acting as an intermediary in this chain extracts a toll, commonly referred to as correspondent fees. These deductions are often unpredictable, meaning the sender cannot accurately calculate the exact amount the recipient will receive. Furthermore, the most significant capital drain occurs during the currency conversion phase. Traditional banks rarely offer the mid-market rate—the true interbank rate found on global financial indices. Instead, they apply a retail markup, creating a massive margin that severely impacts the purchasing power of the remitted funds. Individuals looking to identify and eliminate hidden bank fees must scrutinize the spread between the interbank rate and the rate offered by their institution.

Beyond the financial cost, the legacy system is inherently sluggish. Because money must physically cross borders through multiple jurisdictions and clearing houses, transactions can take anywhere from three to five business days to clear. If a transaction falls on a weekend or a public holiday in any of the involved jurisdictions, the delay is exacerbated. This systemic inefficiency highlights the urgency for a structural overhaul. A rigorous money transfer comparison between legacy banks and decentralized platforms reveals that traditional institutions rely on information asymmetry to maintain their profit margins, penalizing the very individuals who depend on cross-border liquidity the most.

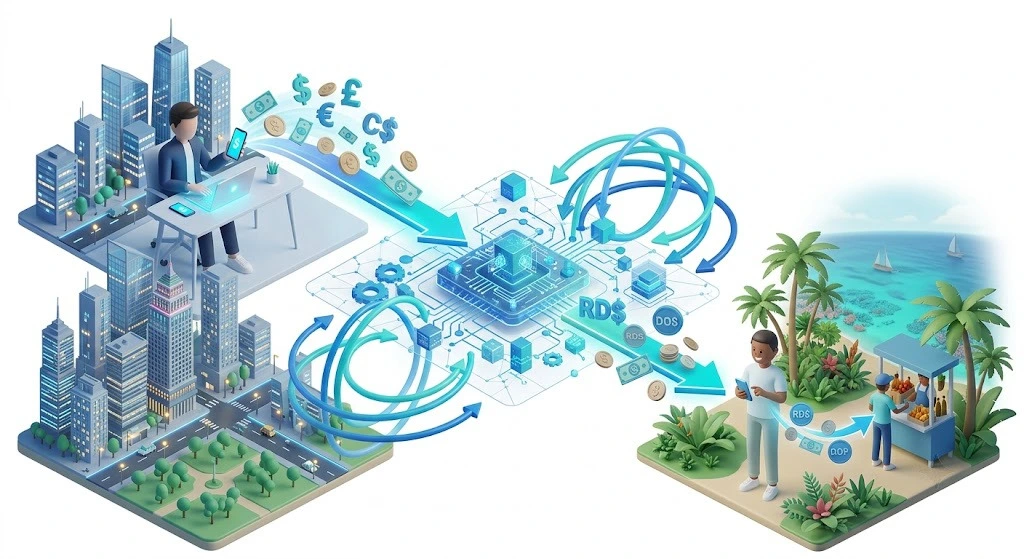

The solution to the archaic correspondent banking system lies in fundamentally altering how currency moves—or more accurately, ensuring that currency does not physically move across borders at all. The CashSwap Club platform operates on a sophisticated Peer-to-Peer (P2P) matching model. In this ecosystem, the underlying principle is local clearing. Capital remains within its respective geographic and jurisdictional boundaries, entirely bypassing the SWIFT network and its associated friction.

The platform facilitates this by providing secure, multi-currency wallets denominated in major global currencies, specifically EUR, USD, GBP, and CAD. Transactions on the marketplace occur exclusively between these same-currency wallets. For instance, if an individual in Europe wishes to send value to the Dominican Republic, the platform's algorithm matches this user with another entity moving capital in the opposite direction. The digital assets are transferred instantly between the EUR or USD wallets within the closed-loop system of the platform. By bypassing traditional chokepoints, individuals who understand the fundamental advantages of P2P ecosystems can leverage the true interbank exchange rate, paying only a minimal, transparent fixed fee for the matching service.

Simultaneously, the corresponding flows in local currencies (such as the Dominican Peso) are executed off-platform through domestic bank transfers or localized payment solutions. Because a domestic transfer in the Dominican Republic is instantaneous and generally free of charge, and a domestic SEPA transfer in Europe operates under the same conditions, the total cost of the transaction plummets. This revolutionary method ensures absolute transfer transparency, as both the sender and the receiver know the exact parameters of the exchange before initiating the match.

This architectural shift is not merely an incremental improvement; it is a systemic redesign. The reliance on local liquidity pools mirrors the efficiency of modern decentralized networks. Observers of financial technology trends frequently note how distributed ledger logic and P2P networks are converging to create the ultimate infrastructure for global financial inclusion. The marketplace does not act as a traditional market maker taking a spread; it simply provides the secure venue and algorithmic efficiency to connect supply with demand.

Transitioning from traditional banking to a P2P marketplace requires an understanding of the operational flow. The CashSwap Club application has been designed to minimize friction while maximizing control for the end-user. The process of optimizing exchange rates to regions like the Dominican Republic follows a highly structured, logical sequence.

Phase 1: Registration and Wallet Capitalization

Upon completing the mandatory security onboarding, users gain access to their multi-currency dashboard. The first step requires funding the appropriate wallet (EUR, USD, GBP, or CAD). This capitalization is performed via standard, low-cost domestic transfer methods. Once the funds reflect in the digital wallet, the user is positioned to interact with the global marketplace.

Phase 2: Initiating the Matching Request

The user configures the desired transaction parameters, specifying the amount, the originating currency, and the target currency requirements. The platform's matching engine scans the global order book to find a counterparty with a mirrored requirement. Because the matching occurs strictly at the mid-market rate, users avoid the exploitative spreads applied by high-street banks. For individuals conducting a marketplace vs local branch cost analysis, this phase demonstrates the most substantial financial savings.

Phase 3: Off-Platform Local Settlement

Once the algorithm secures a match, the digital assets within the platform's multi-currency wallets are temporarily locked by a smart escrow mechanism. Simultaneously, the counterparties execute the local currency transfer off-platform using their respective domestic banking applications. In the context of the Dominican Republic, this means utilizing local banking rails that process transfers instantaneously and without international tariffs.

Phase 4: Verification and Rating

The transaction concludes when both parties confirm the receipt of the off-platform local funds. Upon mutual confirmation, the platform unlocks and credits the digital multi-currency wallets. Crucially, the system mandates an evaluation phase. Each participant must rate the counterparty. This compulsory feedback loop ensures accountability, permanently incentivizing rapid execution and honest interaction within the community.

The primary concern for individuals transitioning away from legacy banks is the assurance of financial security. A decentralized matching model requires a robust, centralized compliance framework to prevent abuse, fraud, and illicit activities. The CashSwap Club platform is engineered with institutional-grade security protocols, designed to exceed the regulatory requirements established by international financial authorities.

The foundation of this secure ecosystem is the strict implementation of Know Your Customer (KYC) and Anti-Money Laundering (AML) directives. Before any user can capitalize a multi-currency wallet or initiate a matching request, they must undergo comprehensive biometric and documentary verification. This stringent onboarding process ensures that every participant on the marketplace is a verified, legitimate entity. By maintaining a closed, highly vetted environment, the platform effectively mitigates the risks typically associated with anonymous peer-to-peer digital networks.

Furthermore, the structural design of the platform inherently protects the users' capital. Because the multi-currency funds remain within the platform's secure escrow architecture until the off-platform local transfer is explicitly verified by both parties, neither participant is exposed to unilateral default risk. If a dispute arises regarding the local off-platform settlement, the funds within the platform's multi-currency wallets remain frozen until the compliance and arbitration team resolves the conflict using verifiable banking receipts.

Trust, however, is not built solely on algorithms and compliance checks; it requires a foundational ethos. The platform operates on principles of community solidarity, financial transparency, and economic empowerment. To understand the deeper philosophical driving forces behind this ecosystem, one can read the foundational principles and economic vision that govern the platform's operations. The mandatory mutual rating system acts as a decentralized reputation ledger, where users build a digital track record of reliability. Bad actors are swiftly marginalized and excised from the network, ensuring that the active user base consists exclusively of trusted, efficient counterparties.

Sending money to the Dominican Republic, or any other global destination, should not entail surrendering a significant portion of capital to legacy institutions that rely on outdated technology and exploitative pricing models. By leveraging a multi-currency, peer-to-peer matching marketplace, individuals reclaim total control over their wealth. The elimination of cross-border physical transfers, combined with domestic off-platform settlements and an unwavering commitment to the real interbank exchange rate, creates a mathematically superior method for global remittances. It is time to abandon the hidden fees of the past and participate in a transparent, community-driven financial ecosystem. The democratization of international finance is active, verifiable, and available.

Because the platform matches users within the ecosystem and relies on domestic banking networks for the local currency settlement, the timeframe is remarkably compressed. Once a match is algorithmically confirmed, the off-platform local transfer and subsequent platform verification generally take only a few minutes to a few hours, completely bypassing the multi-day delays inherent in the traditional SWIFT system.

Hidden bank fees primarily consist of the spread—the difference between the true interbank market rate and the inflated retail exchange rate the bank offers. Additionally, traditional banks pass along unpredictable correspondent network fees. CashSwap Club completely eliminates these by utilizing the mid-market rate for all matches and avoiding the correspondent banking network entirely through localized, off-platform clearing.

Absolutely. The platform operates under strict adherence to international Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Every participant undergoes rigorous identity verification before accessing the marketplace. Furthermore, the escrow-style holding of multi-currency wallets ensures that funds are protected until both parties confirm the successful settlement of the off-platform local transaction.

The platform's architecture is designed to prevent unilateral loss. When a match is initiated, the equivalent multi-currency funds on the platform are securely locked. If a counterparty fails to execute the off-platform local transfer, the locked funds are not released. A dedicated arbitration team steps in to request verifiable banking receipts. If a breach of contract is proven, the funds are returned to the rightful owner, and the offending party is permanently banned from the community, safeguarding the network's integrity.

Our peer-to-peer currency exchange and money transfer platform is currently under development. We are preparing a solution that will allow you to exchange currencies with a seamless and secure experience.

To be among the first to know and not miss anything about the launch, join the club by subscribing to our newsletter.

Visuals disclosure : In the interest of transparency, please note that the images illustrating this article were created using artificial intelligence (AI) generation tools.

© CashSwap Club 2026 - All rights reserved

Designed with ❤️ in Paris • Made in France 🇫🇷

Spanish

Spanish